How Evergreen Funds Make it Easier to Get into Private Markets

Open-ended fund structures are revolutionizing private equity investing — offering lower barriers, inherent diversification, and continuous growth.last updated Tuesday, July 21, 2026

#Evergreen funds #private equity evergreen funds

| | by Sidra Jabeen | Content Manager, Paperfree Magazine |

QUICK LINKS

AD

Get Access to Real Estate Investment Opportunities

Private markets have long been the playground of institutional giants — pension funds, endowments, and ultra-high-net-worth families with the patience to lock up capital for a decade or more. But a structural shift is underway. Evergreen funds, also known as open-ended or semi-liquid funds, are rapidly dismantling the barriers that kept most investors on the sidelines.

In 2025 alone, evergreen fund structures attracted record inflows, with firms such as Hamilton Lane, KKR, Blackstone, and Apollo expanding their open-ended product lineups. According to SEI, the number of evergreen private market vehicles has more than doubled since 2020, and assets under management in these structures now exceed $350 billion globally.

So what exactly are evergreen funds, why are they gaining momentum so quickly, and — most importantly — should they have a place in your portfolio? This guide breaks it all down.

What is an evergreen fund?

An evergreen fund is an open-ended investment vehicle that accepts new capital on a rolling basis and reinvests proceeds back into the portfolio rather than distributing them to investors. Unlike traditional closed-ended private equity funds that have a fixed life of 10 to 12 years, evergreen funds have no predetermined termination date.

The term "evergreen" captures the idea of perpetual growth: capital flows in, gets deployed, generates returns, and those returns are recycled into new investments — creating a continuous compounding loop.

Most evergreen funds in the private markets space are structured as semi-liquid vehicles, meaning they offer periodic redemption windows — typically quarterly or semi-annually — subject to certain limits and notice periods. This is a critical distinction from daily-liquid mutual funds or ETFs. Investors get more flexibility than a traditional drawdown fund, but not the on-demand liquidity of public markets.

Evergreen funds vs. traditional closed-ended funds

Understanding the structural differences between evergreen and traditional private equity funds is essential before making allocation decisions. The table below summarizes the key distinctions.

| Feature | Traditional Closed-Ended Fund | Evergreen (Open-Ended) Fund |

|---|---|---|

| Fund life | 10–12 years fixed | No set end date (perpetual) |

| Capital deployment | Gradual over 3–5 years via capital calls | Immediately upon subscription |

| Liquidity | Illiquid until exit events | Quarterly or semi-annual redemption windows |

| Minimum investment | Often $5M–$10M+ | Typically $50K–$250K |

| J-curve effect | Pronounced, early negative returns are common | Minimized or eliminated |

| Cash flow management | Unpredictable capital calls and distributions | More predictable; no capital call uncertainty |

| Diversification | Concentrated in a single vintage year | Spread across multiple vintages and strategies |

| Performance metric | IRR (Internal Rate of Return) | TWR (Time-Weighted Return) |

| Compounding | Distributions returned to the investor to redeploy | Returns automatically reinvested within the fund |

Why Evergreen Funds are surging | Evergreen Fund vs Closed-end Fund

Several converging forces explain the rapid growth of evergreen structures.

1. Democratization of private markets

The private equity industry has been on a multi-year push to broaden its investor base. As traditional fundraising from institutions becomes more competitive, managers are turning to the high-net-worth and mass-affluent segments for growth. Evergreen structures, with their lower minimums and simplified mechanics, are the preferred vehicle for reaching these investors.

BNP Paribas Wealth Management notes that evergreen funds represent "the most significant innovation in private markets distribution in a generation," allowing wealth managers to allocate client portfolios to alternatives without the operational complexity of managing capital call schedules across dozens of accounts.

2. The J-curve problem, solved

One of the most cited pain points of traditional private equity is the J-curve — the pattern in which fund returns dip into negative territory in the early years as management fees are charged against undeployed capital before investments mature and generate gains.

Evergreen funds largely eliminate this effect. Because capital is deployed immediately into a diversified portfolio that already contains mature, performing assets, new investors benefit from day-one exposure to a seasoned book. There is no multi-year ramp-up period.

3. Built-in compounding

Traditional PE funds distribute proceeds to investors upon exits. Those investors then face a reinvestment challenge: where do they put the capital to maintain their private markets allocation? This gap — the time between receiving a distribution and deploying it into a new fund — creates cash drag that erodes long-term returns.

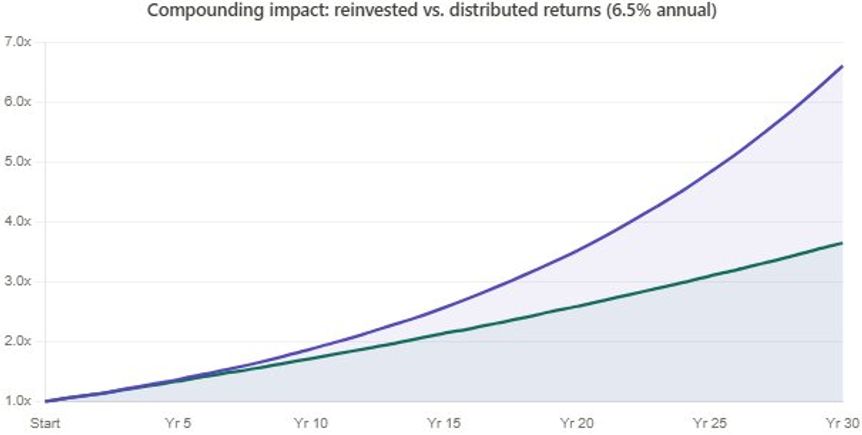

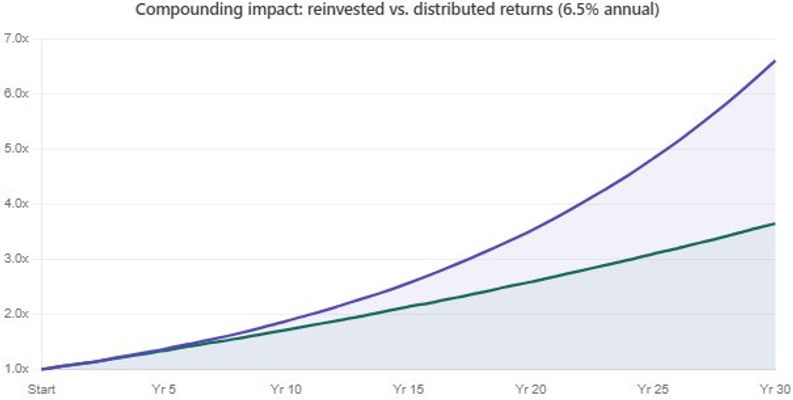

Evergreen funds solve this by automatically reinvesting within the vehicle. According to JP Morgan Asset Management, the impact of this compounding is substantial. Assuming a 6.5% total annual return, reinvested income produces a 6.6x multiple on invested capital (MOIC) over 30 years compared to just 3.6x for distributed income.

4. Operational simplicity

For financial advisors and family offices managing multiple client portfolios, evergreen funds dramatically reduce administrative burden. There are no capital calls to manage, no unpredictable cash flows to forecast, and no complex waterfall distribution calculations. A single subscription gets the investor in. A single redemption request gets them out.

How do evergreen funds fit in your portfolio?

Evergreen funds are not a replacement for traditional closed-ended vehicles. Rather, they serve specific structural roles depending on an investor's experience level and portfolio complexity.

Private Equity Evergreen Funds - For first-time private market investors

If you are new to private markets, an evergreen fund can serve as your entry point. It provides instant diversification across strategies, sectors, geographies, and vintage years — something that would take years and significant capital to achieve through individual closed-ended fund commitments.

The periodic liquidity also provides a psychological comfort layer. Knowing you can access your capital quarterly, even if with some constraints, makes it easier to take the first step into a fundamentally illiquid asset class.

For experienced allocators

Sophisticated investors already managing a portfolio of closed-ended fund commitments can use evergreen funds as a pacing and rebalancing tool. Specific use cases include:

- Maintaining target allocation

When a closed-ended fund distributes capital, the investor's overall PE allocation drops. Rather than waiting months for the next fund commitment, those proceeds can be immediately reinvested into an evergreen vehicle to maintain the target percentage. - Smoothing vintage year exposure

Traditional PE investors often face the challenge of vintage year concentration. If you committed heavily in 2022 but missed 2023, your return profile is hostage to the conditions of a single deployment window. Evergreen funds naturally spread exposure across vintages by continuously deploying capital. - Liquidity management

Evergreen funds act as a liquid reserve within the illiquid allocation, providing optionality to fund future closed-ended commitments or rebalance the broader portfolio.

Best strategies for evergreen funds

Not all private market strategies are equally suited to the evergreen format. The requirement to meet periodic redemptions means the underlying portfolio must generate sufficient liquidity without forcing fire sales.

Private credit funds

Private credit funds are arguably the most natural fit for evergreen structures. The recurring income from loan portfolios — interest payments, origination fees, and principal repayments — provides a steady cash flow that can fund redemptions without selling assets at a discount. The strategy's inherently shorter duration (typically 3 to 5 years per loan) also supports portfolio turnover.

Secondaries

Secondary strategies, which involve buying existing LP interests in mature funds, are another strong match. Because these portfolios are already partially or fully invested, they generate cash from day one through ongoing distributions from the underlying funds. This reduces cash drag—the bane of evergreen structures—and accelerates compounding.

Co-investments and direct equity

Some evergreen funds incorporate co-investments or direct equity positions alongside their core strategy. While these offer higher return potential, they tend to be less liquid and require careful portfolio sizing to ensure the fund can meet redemption obligations.

The compounding advantage: why it matters more than you think

The compounding dynamics within evergreen funds deserve special attention because they are often underestimated.

In a traditional closed-ended fund, when an investment is realized — say a portfolio company is sold — the proceeds are distributed to investors. Those investors must then find a new home for that capital. During the interim, the money sits in cash or low-yielding instruments, earning nothing effectively.

In an evergreen fund, that same exit event triggers an immediate redeployment into the next opportunity within the vehicle. There is zero gap. The capital never stops working.

Over short time horizons (1 to 3 years), the difference is marginal. Over long time horizons (10 to 30 years), it is transformative. JP Morgan's research, illustrating the 6.6x vs. 3.6x MOIC divergence over 30 years, makes the point starkly: the investor who reinvests consistently earns nearly twice the multiple as the one who doesn't.

This is why many advisors now recommend evergreen funds as a core, permanent allocation within the alternatives sleeve — not a tactical trade, but a structural holding designed to compound over decades.

Key risks and caveats

Evergreen funds are not a magic solution. Investors must understand several important limitations.

Liquidity is not guaranteed

While evergreen funds offer periodic redemption windows, they are not the same as daily-liquid vehicles. Most funds cap quarterly redemptions at 5% to 25% of net asset value (NAV). In periods of market stress, when many investors attempt to redeem simultaneously, queues may form. Some funds may gate redemptions entirely during extreme conditions.

Valuation lag

Private market assets are typically valued quarterly. This means NAV-based pricing may not fully reflect current market conditions. During rapidly declining markets, an investor might redeem at a NAV that does not yet capture recent losses — at the expense of remaining investors. Conversely, in rising markets, new subscriptions may dilute existing investors at stale valuations.

Fee structures

Evergreen funds typically charge management fees of 1.0% to 1.5% annually, plus performance fees of 10% to 20% above a hurdle rate. Because there is no end date, management fees compound indefinitely — unlike closed-ended funds, where fees wind down as the fund approaches termination.

Manager quality still matters

A well-structured evergreen vehicle with a poor investment team is still a poor investment. The fund wrapper does not change the fundamental importance of manager selection, investment strategy, and execution quality. Proper due diligence on track record, deal sourcing, and portfolio construction remains essential.

Performance comparison: understanding IRR vs. TWR

One common source of confusion is comparing performance between evergreen and closed-ended funds. The two use different metrics, and direct comparison requires care.

| Metric | Used By | What It Measures | Best For |

|---|---|---|---|

| IRR (Internal Rate of Return) | Closed-ended funds | Return based on the actual timing of cash flows | Evaluating manager's skill in deploying and returning capital |

| TWR (Time-Weighted Return) | Evergreen/open-ended funds | Compound portfolio growth, ignoring cash flow timing | Evaluating ongoing portfolio performance |

| MOIC (Multiple on Invested Capital) | Both | Total value / total invested capital | Cross-structure comparison on a common basis |

For investors benchmarking across both fund types, MOIC provides the most apples-to-apples comparison. It strips out the timing effects that make IRR and TWR non-comparable and simply answers: for every dollar I put in, how many dollars did I get back?

Allocation framework: building a blended portfolio

There is no one-size-fits-all allocation. The right mix depends on your investment experience, liquidity needs, return objectives, and time horizon. The following framework illustrates how the evergreen/closed-ended balance might shift across investor profiles.

| Investor Profile | Evergreen Allocation | Closed-Ended Allocation | Rationale |

|---|---|---|---|

| New to private markets | 70–100% | 0–30% | Maximize diversification and simplicity; learn the asset class |

| Intermediate (3–5 years PE experience) | 40–60% | 40–60% | Blend broad access with targeted, high-conviction bets |

| Advanced (10+ years, complex portfolio) | 20–30% | 70–80% | Evergreen as a pacing tool and liquidity buffer; core returns from closed-ended |

As investors gain experience and comfort with illiquidity, the allocation typically shifts toward closed-ended funds for core return generation, with evergreens maintaining a steady role in portfolio management and compounding.

What to look for when selecting an evergreen fund

Choosing the right evergreen fund requires evaluating several dimensions beyond headline returns.

- Strategy alignment

Does the fund's underlying strategy (private credit, secondaries, buyout, or growth equity) align with your portfolio objectives and existing exposures? - Redemption terms

How frequently can you redeem? What are the notice periods? Are there gates or caps? Understanding these terms is critical — a fund with attractive returns but 12-month notice periods and 5% quarterly caps may not provide the liquidity you expect. - Track record

How long has the fund been operating? What is the vintage diversity of its portfolio? Newer evergreen funds may carry concentration risk if they have not yet diversified across enough investment cycles. - Fee structure

Compare the total expense ratio (management fee + performance fee + fund expenses) against the strategy's expected gross return. A 2.5% total cost on a 10% gross return strategy leaves you with a 7.5% net return — significantly less than you might assume at first glance. - Manager reputation and infrastructure

Does the manager have the operational capability to handle rolling subscriptions, redemptions, and continuous portfolio rebalancing? Evergreen funds are more operationally demanding than closed-ended vehicles, and not all managers have the infrastructure to run them effectively.

Frequently asked questions

1. Are evergreen funds suitable for retirement portfolios?

Evergreen funds can work well within retirement portfolios, particularly for investors with a long time horizon. The compounding mechanism aligns naturally with retirement planning, and the periodic liquidity provides more flexibility than traditional locked-up structures. However, investors should ensure they maintain sufficient liquid assets outside the fund to cover near-term income needs, as redemptions are not instantaneous.

2. How quickly can I access my money from an evergreen fund?

Most evergreen funds offer quarterly redemption windows with 30 to 90 days' notice. However, redemptions are typically subject to caps (often 5% to 25% of fund NAV per quarter). In practice, this means it could take one to four quarters to fully exit a position, depending on fund size and redemption demand. During periods of high redemption volume, queues may extend this timeline further.

3. Do evergreen funds outperform traditional closed-ended PE funds?

Direct performance comparison is difficult because the two structures use different metrics (TWR vs. IRR) and serve different purposes. Generally, top-quartile closed-ended funds may generate higher peak returns due to their concentrated, illiquid nature. However, evergreen funds can deliver competitive, risk-adjusted returns over time, particularly when compounding is factored in. The choice should be driven by portfolio fit and investor needs rather than a pure performance horse race.

4. What happens if an evergreen fund manager performs poorly?

Unlike closed-ended funds that wind down after 10 to 12 years regardless of performance, an underperforming evergreen fund can continue indefinitely. This makes investor vigilance especially important. Most evergreen fund documents include governance provisions that allow a supermajority of investors to vote on the termination of the fund. Practically, though, the primary protection is the ability to redeem at the next available window and reallocate capital elsewhere.

5. Can I combine evergreen and closed-ended funds in the same portfolio?

Absolutely — this is actually the recommended approach for most investors beyond the entry level. Evergreen funds provide broad diversification, compounding, and liquidity management, while closed-ended funds offer access to top-tier managers, illiquidity premia, and concentrated high-conviction strategies. The blend creates a more resilient and flexible private markets portfolio than either structure alone.

The bottom line

Evergreen funds are not a passing trend. They represent a fundamental evolution in how private market exposure is packaged, accessed, and managed. For investors who have been sitting on the sidelines, intimidated by decade-long lockups and multi-million-dollar minimums, evergreen structures offer a credible and compelling on-ramp.

For those already deep in private markets, these vehicles add a layer of portfolio engineering sophistication — enabling smoother pacing, disciplined reinvestment, and tactical liquidity management that closed-ended structures alone cannot provide.

The key is to understand what evergreens are and what they are not. They are powerful structural tools that complement, rather than replace, traditional private equity. Used wisely, they can enhance diversification, amplify compounding, and help maintain allocation discipline through market cycles.

The private markets landscape in 2026 offers more choice and accessibility than ever before. Evergreen funds are a significant reason why.

Sources:

- Moonfare, "Investing in Evergreen Funds? Here's How They Can Fit in Your Portfolio," February 2026

- BNP Paribas Wealth Management, "Investing in Private Markets Through Evergreen Structures"

- SEI, "Evergreen Funds: The Next Frontier in Private Markets"

- Hamilton Lane, "Evergreen Funds" Knowledge Center

- JP Morgan Asset Management, Private Markets Compounding Research

- Barron's, "The Rise of Evergreen Funds"

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice, financial advice, tax advice, or a recommendation to buy or sell any securities or investment products. The information presented here is based on publicly available sources believed to be reliable as of March 2026, but PaperFree.com makes no representations or warranties as to its accuracy, completeness, or timeliness. Private equity and private market investments carry significant risks, including the potential loss of all invested capital. Past performance is not indicative of future results. Evergreen funds are semi-liquid, not fully liquid — redemptions are subject to fund-specific terms, caps, gates, and notice periods. Investors should conduct their own due diligence and consult with a qualified financial advisor, tax professional, or legal counsel before making any investment decisions. PaperFree.com and its contributors do not have any financial interest in the funds or companies mentioned in this article.

Pages Related to #Evergreen funds

- 4 Ways to Better Organize Inventory Management

- [closed] CMF. Cedar Multifamily Fund

![[closed] CMF. Cedar Multifamily Fund](https://d2sv4n3pfes7l9.cloudfront.net/file_paperfree_144_2020-8-21-19-57-p_pf-avatar.jpg)

- EB-5 for Tech Entrepreneurs: Immigration Program for Startup Founders | Paperfree

- EB5 Visa Bulletin June 2025: Priority Dates & Filing Updates

- Indian EB-5 Golden Visa Applicants

- Investments

- Fee increase for EB-5 U.S. Golden Visa 2024

- USA EB5 visa consultant

Popular Page

Private Real Estate Funds - Investments to Drive Income and Capital Growth

Book a Free Complimentary Call

Search within Paperfree.com

real estate investing Investment Visa USA Investment Magazine Private Real Estate Funds real estate funds