Assets vs Liabilities: Your Complete Investment Strategy Guide

Understanding the Foundation of Wealth Building and Financial Freedomlast updated Tuesday, July 21, 2026

#asset vs liabilities #assets and liabilities list

| | by Sidra Jabeen | Content Manager, Paperfree Magazine |

QUICK LINKS

AD

Get Access to Real Estate Investment Opportunities

Building lasting wealth begins with understanding one fundamental principle: the difference between assets and liabilities. This distinction forms the cornerstone of every successful investment strategy and determines whether you're moving toward financial freedom or staying trapped in the cycle of debt.

Discover data-driven, AI-enhanced investment and financing solutions tailored to your needs. Connect with Paperfree today and take control of your financial future!

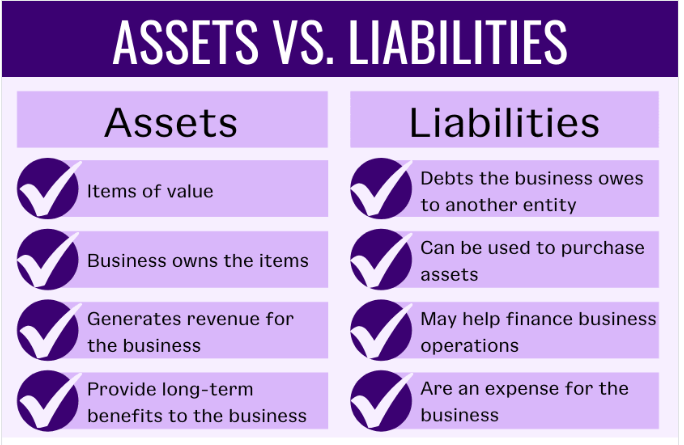

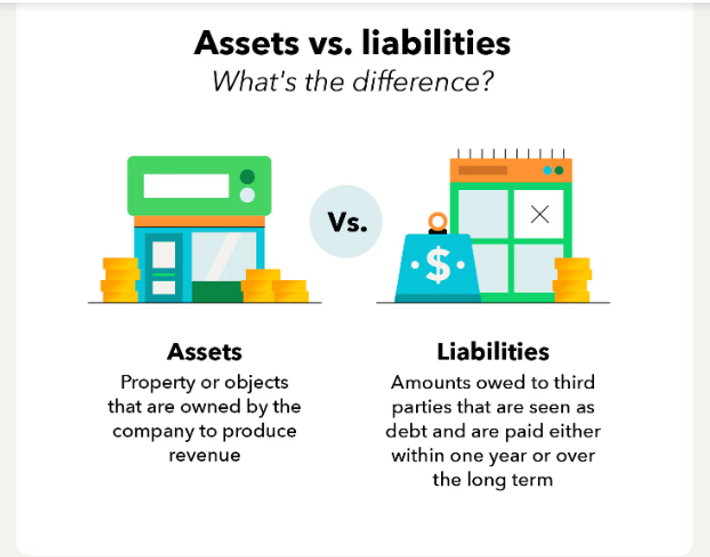

What Are Assets and Liabilities?

Assets are resources that put money into your pocket. They generate income, appreciate, or provide financial benefits over time. Think of assets as your wealth-building tools that work for you even while you sleep.

Liabilities, on the other hand, take money out of your pocket. They require ongoing payments, depreciate, or create financial obligations that drain your resources. While some liabilities are necessary, understanding their impact is crucial for financial success.

Common Examples of Assets

Real estate investment properties generate rental income and typically appreciate over time. Stocks and bonds offer dividends and potential capital gains. Business ownership creates multiple income streams. Retirement accounts like 401(k)s and IRAs grow tax-advantaged. Intellectual property, such as patents, books, or courses, generates passive royalties. High-yield savings accounts and certificates of deposit provide guaranteed returns.

Common Examples of Liabilities

Consumer debt, including credit cards and personal loans, charges high interest rates. Auto loans depreciate as vehicles lose value. Student loans require monthly payments without generating income. Mortgages on primary residences demand ongoing payments (though they can become assets through appreciation). Unnecessary subscriptions and memberships drain cash monthly.

The Golden Rule of Wealth Building

Successful investors follow one simple principle: acquire assets that generate income and minimize liabilities that create expenses. Your net worth grows when your assets outpace your liabilities. Every financial decision should be evaluated through this lens.

This golden rule separates the wealthy from those who struggle financially. Wealthy individuals understand that true financial freedom comes not from earning a high salary but from building a portfolio of assets that work continuously to generate income.

A doctor earning $300,000 annually but spending $290,000 on liabilities is less financially secure than a teacher earning $60,000 who invests $20,000 yearly in income-producing assets.

The math of asset vs liabilities is straightforward: if your assets generate more money than your liabilities consume, you achieve positive cash flow. This surplus can be reinvested to acquire more assets, creating a virtuous cycle of wealth accumulation.

Each new asset purchased increases your income capacity, while each liability eliminated frees up more cash to buy additional assets.

Consider every purchase through this lens. Before buying anything, ask yourself: "Is this an asset that will put money in my pocket, or a liability that takes money out?" A $50,000 luxury car is a liability requiring insurance, fuel, maintenance, and depreciation. That same $50,000 invested in dividend stocks yielding 4% generates $2,000 annually—money that continues growing through reinvestment.

This principle also applies to time investments. Spending hours learning marketable skills or building a side business creates intangible assets that increase your earning potential. Conversely, excessive time spent on consumption—shopping, scrolling social media, or watching television—represents opportunity costs where you could be building wealth.

The power of this rule compounds over time. In year one, you might struggle to save $5,000 for your first investment. But as your assets grow and generate returns, you'll find it easier to save $10,000 in year two, then $20,000 in year three. Meanwhile, eliminating liabilities frees up even more capital. This exponential growth is how ordinary people achieve extraordinary wealth.

7 Investment Strategies to Maximize Assets and Minimize Liabilities

1. Create Multiple Income Streams

Don't rely on a single paycheck. Diversify your income sources by investing in dividend-paying stocks, rental properties, online businesses, or freelance work. Multiple streams provide security and accelerate wealth accumulation.

2. Adopt the 50-30-20 Budget Rule

Allocate 50% of your income to necessities, 30% to wants, and 20% to savings and investments. This framework ensures you're consistently building assets while managing liabilities responsibly.

3. Eliminate High-Interest Debt First

Credit card debt and payday loans are wealth destroyers. Use the debt avalanche method by paying off the highest-interest debts first while making minimum payments on others. This mathematical approach saves thousands in interest.

4. Invest in Appreciating Assets Early

Time is your greatest ally in investing. Start contributing to retirement accounts in your 20s or 30s to harness compound interest. Even small monthly contributions grow substantially over decades.

5. Turn Liabilities into Assets

Consider house hacking by renting out rooms in your primary residence to offset mortgage payments. Lease vehicles you can write off for business purposes. Transform necessary expenses into income-generating opportunities.

6. Build an Emergency Fund

Maintain three to six months of expenses in a high-yield savings account. This asset protects you from taking on debt during emergencies and provides peace of mind for aggressive investing.

7. Continuously Educate Yourself

Financial literacy is an asset that pays dividends forever. Read investment books, follow market trends, attend seminars, and learn from successful investors. Knowledge prevents costly mistakes and reveals opportunities.

Smart Asset Allocation by Age

In your 20s and 30s

Focus on growth assets with 80-90% in stocks and equity funds. Take calculated risks while you have time to recover from market downturns. Prioritize eliminating student loans and building credit.

In Your 40s and 50s

Shift to 60-70% stocks and 30-40% bonds for balanced growth and stability. Maximize retirement contributions and consider real estate investments. Pay off your mortgage aggressively.

In Your 60s and Beyond

Move to conservative allocations with 40-50% stocks and 50-60% bonds and fixed income. Preserve capital while generating steady income streams. Eliminate all remaining liabilities before retirement.

Complete Assets and Liabilities List: Categorize Your Finances

Understanding your complete financial picture requires a comprehensive assets and liabilities list. Use this detailed breakdown to audit your own finances and identify opportunities for improvement.

Personal Assets List

Liquid Assets

Cash in checking accounts, savings accounts, money market accounts, certificates of deposit (CDs), treasury bills, and emergency funds.

Investment Assets

Individual stocks, mutual funds, index funds, ETFs, bonds, cryptocurrency, precious metals (gold, silver), and commodities.

Retirement Assets

401(k) accounts, traditional IRAs, Roth IRAs, pension plans, 403(b) accounts, SEP IRAs, and annuities.

Real Estate Assets

Rental properties, investment properties, real estate investment trusts (REITs), commercial property, and land held for appreciation.

Business Assets

Business ownership equity, partnership stakes, sole proprietorship assets, intellectual property, patents, trademarks, copyrights.

Personal Property Assets

Valuable collectibles (art, antiques, coins), jewelry, vehicles (if appreciating classics), and equipment that generates income.

Income-Generating Assets

Royalties from books or music, affiliate marketing websites, dividend-paying investments, peer-to-peer lending accounts, vending machines, and storage unit facilities.

Personal Liabilities List

Consumer Debt

Credit card balances, personal loans, payday loans, buy-now-pay-later balances, and retail store credit cards.

Educational Debt

Federal student loans, private student loans, parent PLUS loans, and educational lines of credit.

Housing Liabilities

Primary residence mortgage, home equity loans, home equity lines of credit (HELOC), property taxes owed, and HOA fees.

Vehicle Liabilities

Auto loans, motorcycle loans, boat loans, RV loans, and lease obligations.

Business Liabilities

Business loans, business credit cards, equipment financing, commercial mortgages, accounts payable.

Tax Liabilities

Unpaid income taxes, back taxes, tax penalties, and estimated tax payments are owed.

Other Liabilities

Medical bills, legal judgments, alimony or child support obligations, co-signed loans, and personal guarantees.

How to Use Your Assets and Liabilities List

Create a spreadsheet with three columns: Item, Current Value, and Category. List every asset with its current market value and every liability with the outstanding balance. Update this list quarterly to track your financial progress. Calculate your net worth by subtracting total liabilities from total assets—this number should grow consistently.

Identify liabilities costing more than 7% interest for immediate payoff priority. Look for underperforming assets that could be redirected to higher-return investments. This assets and liabilities list becomes your financial roadmap, showing exactly where you stand and where you need to go.

Common Investment Mistakes to Avoid

Treating your primary residence as your main investment is risky because it doesn't generate cash flow. Keeping too much cash in low-interest accounts loses purchasing power to inflation. Ignoring tax-advantaged accounts means giving up free money from employer matches. Buying depreciating assets on credit compounds financial damage. Following trends without research leads to poor investment decisions.

The Psychology of Asset Building

Successful investing requires discipline and delayed gratification. Learn to distinguish between wants and needs. View purchasing decisions through the lens of opportunity cost—every dollar spent on liabilities is a dollar that can't work for you as an asset.

Cultivate an abundance mindset focused on growing your asset column rather than a scarcity mindset that leads to debt accumulation. Surround yourself with financially successful people who inspire better money habits.

Tracking Your Asset-to-Liability Ratio

Calculate your net worth quarterly by subtracting total liabilities from total assets. Watch this number grow over time as proof of your wealth-building progress. Use apps like Mint, Personal Capital, or YNAB to automate tracking.

Set specific goals such as increasing net worth by 20% annually or reducing liabilities by $10,000 yearly. Measurable targets keep you accountable and motivated.

Take Action Today

Start by listing all your assets and liabilities to understand your current financial position. Identify one liability you can eliminate within six months and one asset you can acquire this quarter. Small, consistent actions compound into significant wealth over time.

Remember that building wealth is a marathon, not a sprint. Focus on making progress rather than achieving perfection. Every positive financial decision moves you closer to financial independence.

Book a Free Consultation with Paperfree's Expert Financial Advisor Today! Get personalized advice to secure your financial future, all with no obligation. Don't wait – take the first step toward financial clarity now!

Frequently Asked Questions

Q1: Can my home be considered an asset or a liability?

Your primary residence is typically a liability because it requires mortgage payments, property taxes, insurance, and maintenance without generating income. However, it can become an asset if you rent out portions of it, if it appreciates significantly in value, or once it's paid off and reduces your living expenses. Investment properties that generate positive cash flow are true assets.

Q2: How much should I invest in assets versus paying off liabilities?

Focus on eliminating high-interest debt (anything above 7-8% interest) before aggressive investing. Simultaneously, always contribute enough to retirement accounts to capture full employer matching—that's an immediate 100% return. Once high-interest debt is cleared, split your available funds between moderate debt repayment and building your investment portfolio.

Q3: What's the fastest way to start building assets with limited income?

Begin with micro-investing apps that allow contributions as small as $5. Open a high-yield savings account and automate even small transfers. Invest in yourself through skills that increase earning potential. Consider side hustles that convert your time into income-generating assets. Focus on consistency rather than amount—small investments grow substantially over time through compound interest.

Q4: Are all debts considered bad liabilities?

No, not all debt is equal. "Good debt" includes low-interest loans used to acquire appreciating assets like real estate or to invest in education that significantly increases earning potential. "Bad debt" includes high-interest consumer loans for depreciating items like cars, electronics, or vacations. The key is whether the debt helps build wealth or diminishes it.

Q5: How do I know if I'm making good investment decisions?

Track your net worth monthly and ensure it's growing over time. Diversify across different asset classes to reduce risk. Educate yourself continuously about investment principles. Consider working with a fee-only fiduciary financial advisor who's legally obligated to act in your best interest. Good investments align with your risk tolerance, time horizon, and financial goals while consistently building wealth.

Pages Related to #asset vs liabilities

- Wealth Building & Preservation: Investments & Loans | Paperfree

- Insurance Sales Tips

- How to create a buyer persona: 63 buyer persona questions to know.

- What is a Buyer Persona? [video]

- 7 B2B Marketing Strategies Examples For Long-term Success

- Five Steps To Making Sales Through Social Media

- LinkedIn lead generation. 3 Simple Steps that can Swiftly Increase Linkedin Lead Generation

- How to use LinkedIn effectively as a personal CRM system

Popular Page

Private Real Estate Funds - Investments to Drive Income and Capital Growth

Book a Free Complimentary Call

Search within Paperfree.com

real estate investing Investment Visa USA Investment Magazine Private Real Estate Funds real estate funds