Can Semi-Liquid Funds Fuel Evergreen Compounding Returns?

How evergreen private-equity vehicles turbo-charge long-term growth with periodic liquidity.last updated Friday, July 17, 2026

#Semi-Liquid Funds #Semi liquid funds examples

| | by Sidra Jabeen | Content Manager, Paperfree Magazine |

QUICK LINKS

AD

Get Access to Real Estate Investment Opportunities

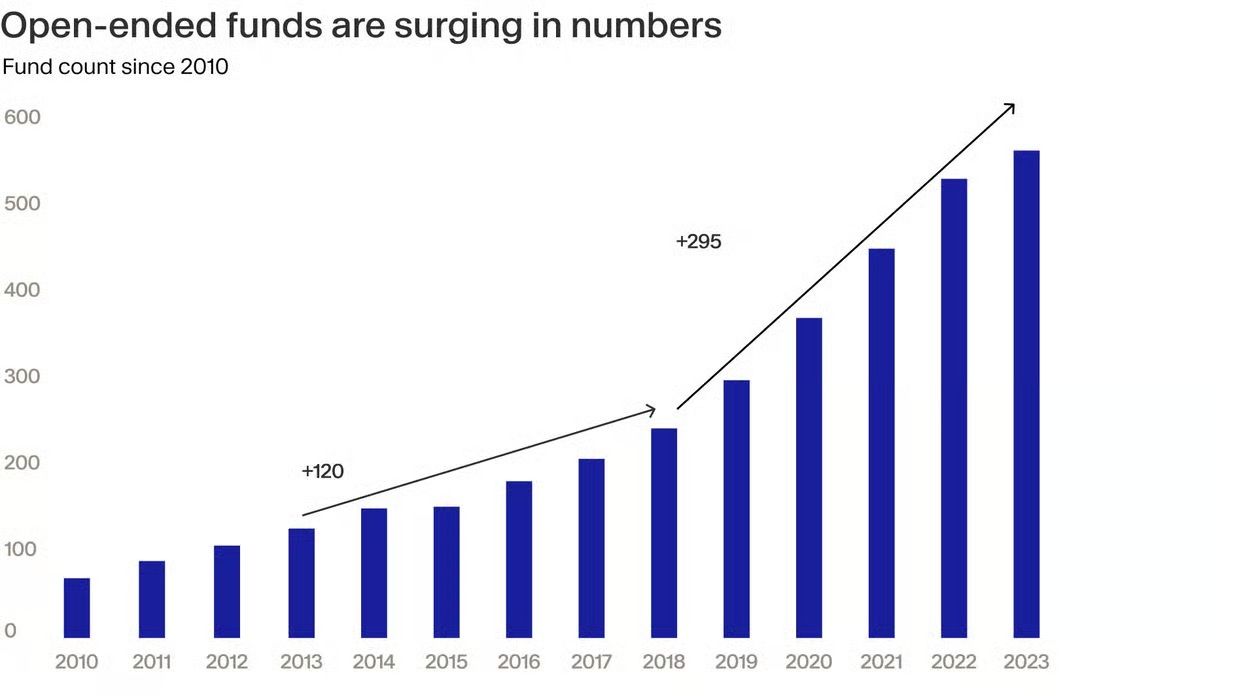

The private equity landscape is witnessing an unprecedented transformation. Traditional closed-end funds, with their decade-long capital lock-ups, are being challenged by innovative semi-liquid structures that promise institutional-grade returns with enhanced flexibility. With over $400 billion in cumulative net asset value across private market evergreen funds since 2019 and record-breaking growth to $350 billion by 2024, these vehicles are reshaping how investors access private markets.

But the critical question remains: can these evergreen vehicles truly deliver superior compounding returns while maintaining investor liquidity? The evidence suggests they can—and the mathematics behind their success story is compelling.

Let's explore:

What Are Semi-Liquid Funds?

Semi-liquid funds, also known as evergreen or open-ended funds, represent a revolutionary hybrid investment structure that eliminates the traditional constraints of private equity investing. Unlike conventional PE funds with predetermined lifespans, these perpetual vehicles operate indefinitely, offering investors periodic redemption opportunities while maintaining sophisticated long-term capital deployment strategies.

Defining characteristics of semi-liquid funds:

- Evergreen structure with no predetermined termination date.

- Quarterly or monthly liquidity windows (typically capped at 5% of fund NAV).

- Immediate portfolio exposure upon investment.

- Continuous capital recycling and reinvestment.

- Lower minimum investment thresholds ($25,000-$100,000 vs. $1-5 million).

- Diversified exposure across sectors, strategies, and vintage years.

The mid-year Private Equity 2025 report and analysis are now available. Click here to read the complete analysis by PaperFree.

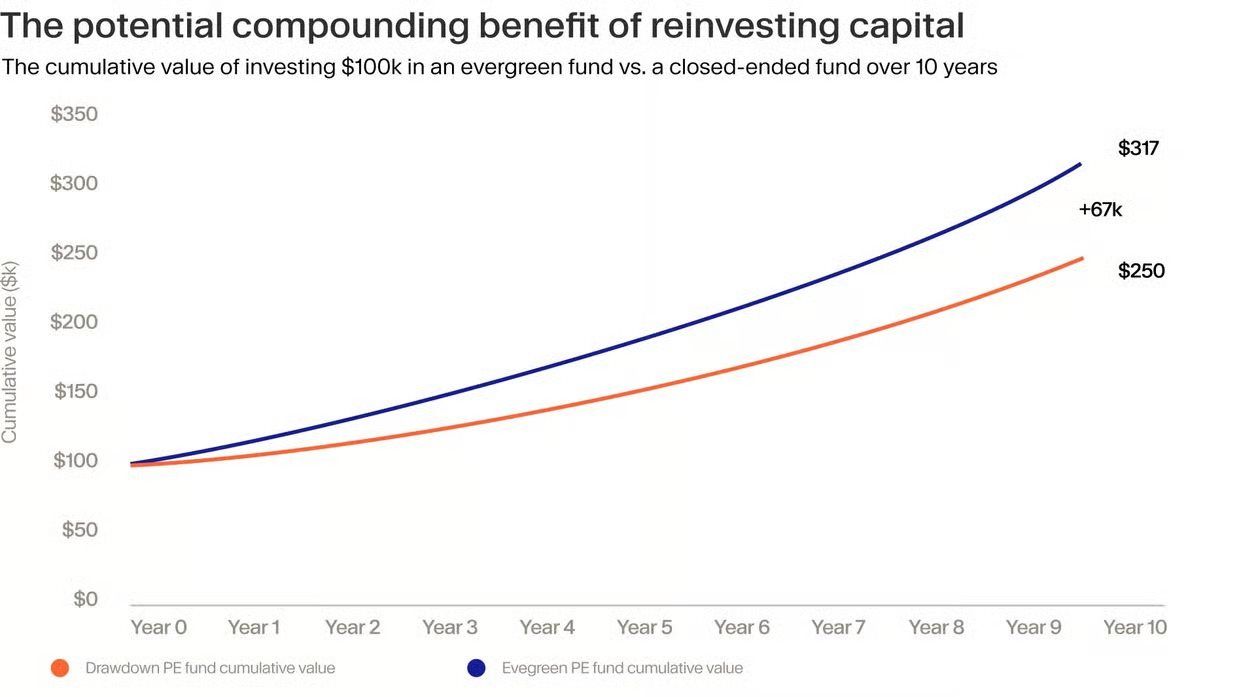

The Mathematical Advantage: How Compounding Transforms Returns

The power of compounding in semi-liquid funds extends far beyond traditional reinvestment strategies. According to KKR's financial modeling, these structures can achieve a 3x multiple of invested capital (MOIC) from an 11.6% net IRR over a 10-year horizon. To achieve the exact 3x multiple, a traditional closed-ended fund would require a substantially higher 18.4% IRR.

How Does the Compounding Effect Work?

The compounding effect is one of the most powerful wealth-building concepts in investing, often called "the eighth wonder of the world" because of its remarkable ability to transform modest initial investments into substantial wealth over time.

The Basic Mechanism

At its core, compounding works through a simple but powerful principle: you earn returns on both your original investment and on all the returns you've already earned. This creates what experts describe as "a virtuous circle where your capital increases in size, which increases the income you receive, which once again increases the capital".

Think of it like planting a tree that produces fruit. It's like planting a seed that keeps growing more trees, each giving you more fruit year after year. Each year, you not only get fruit from your original tree, but also from all the new trees that grew from the seeds of previous harvests.

How It Works in Practice

When the value of your investments goes up, your account balance increases. As long as you leave the gains invested, your returns have the opportunity to compound over time.

Here's how this differs from simple interest:

Simple Interest: You only earn returns on your original investment

- Year 1: $10,000 × 6% = $600 return

- Year 2: $10,000 × 6% = $600 return

- Year 3: $10,000 × 6% = $600 return

Compound Interest: You earn returns on your original investment, PLUS all accumulated returns

- Year 1: $10,000 × 6% = $600 → Total: $10,600

- Year 2: $10,600 × 6% = $636 → Total: $11,236

- Year 3: $11,236 × 6% = $674 → Total: $11,910

Notice how each year's return gets larger because you're earning returns on a bigger base amount.

The Reinvestment Process

Compounding involves reinvesting any returns over the lifespan of a position so that income received from it is transformed into additional investment capital. This means:

- Dividends get reinvested instead of being taken as cash

- Interest payments are added back to the principal

- Capital gains remain in the investment to grow further

- All returns become part of your new, larger investment base

Why Time Matters Most

The longer you save or invest your money, the more your returns can grow. This is because starting early allows your investments to compound over a longer period.

The power becomes more pronounced over time because the earlier your money starts compounding, the more pronounced the effect will be. This creates an exponential growth curve rather than a linear one.

Real-World Applications of Compounding Effect

- In Mutual Funds and ETFs

You earn returns on both the initial lump sum investment and the reinvested dividends, essentially receiving interest on the interest. Many funds automatically reinvest dividends, making compounding seamless. - In Semi-Liquid Funds

These funds harness compounding by automatically reinvesting profits from successful exits back into new investments, rather than distributing them to investors who might delay reinvestment. - In Retirement Accounts

401(k)s and IRAs are explicitly designed to maximize compounding by deferring taxes on gains, automatically reinvesting returns, and preventing early withdrawals that would interrupt the compounding process.

Key Factors That Enhance Compounding

- Rate of Return

The larger your investment return, the bigger the difference that compounding can make - Time Horizon

The longer you let compounding work, the more dramatic the results - Consistency

Regular contributions amplify the effect through dollar-cost averaging - Reinvestment

Never taking distributions allows the full power of compounding to work

The Mathematical Reality

Wealth creation is typically the get-rich-slowly kind, powered by compounding. Unlike lottery winners or crypto speculators, most lasting wealth comes from the patient application of compounding principles over decades.

The mathematics is straightforward, but the results are extraordinary:

- 10 years: Modest but noticeable growth

- 20 years: Significant wealth accumulation

- 30+ years: Potentially life-changing wealth creation

The compounding effect works because it harnesses exponential rather than linear growth. Each period's returns become part of the base for the next period's calculations, creating an accelerating snowball effect that becomes more powerful with time. This is why financial advisors emphasize starting early, staying consistent, and avoiding the temptation to interrupt the compounding process through early withdrawals or market timing attempts.

Immediate Capital Deployment: Eliminating the J-Curve Effect

Traditional private equity funds suffer from the notorious "J-curve" effect, where committed capital sits idle during the investment period, generating negative returns initially due to fees and gradual deployment. Semi-liquid funds eliminate this inefficiency through several mechanisms:

Capital Efficiency Advantages:

- Instant Portfolio Exposure

New subscriptions are immediately invested at current NAV into existing diversified portfolios. - No Capital Drag

Eliminates the waiting period where committed capital earns minimal returns. - Continuous Reinvestment

Proceeds from successful exits are immediately redeployed rather than distributed. - Full Capital Utilization

Maintains fully invested positions across market cycles.

Diversification Benefits:

Semi-liquid funds provide immediate exposure to diversified portfolios spanning various sectors, investment strategies, and vintage years. This instant diversification offers a significant advantage over traditional funds, which require investors to commit to multiple vintage years to achieve a similar risk distribution.

Quarterly Liquidity: Flexibility with Intelligent Constraints

The semi-liquid nature of these funds addresses one of private equity's most significant limitations while maintaining the discipline necessary for long-term value creation. The liquidity framework includes sophisticated mechanisms designed to protect long-term compounding potential:

Liquidity Management Framework:

- Redemption Caps

Typically limited to 5% of fund NAV per period. - Notice Periods

Usually, 60-90 days' advance notification is required. - Quarterly Windows

Predetermined redemption opportunities, often monthly or quarterly. - Gating Rights

Fund managers can temporarily suspend redemptions during market stress. - Liquidity Sleeves

Portion of assets held in cash or public securities to facilitate redemptions.

Risk Management Considerations:

The "semi-liquid" designation underscores a critical limitation—these funds are not fully liquid like public securities. Redemptions remain subject to notice periods, predetermined windows, and fund-level caps, making them suitable for capital that can be committed for extended periods despite periodic liquidity features.

Performance Analysis: Semi-Liquid vs. Traditional Structures

Industry data reveals compelling performance characteristics that support the semi-liquid fund thesis:

Return Profile Comparison:

- Semi-liquid PE funds: Targeting 11-15% net IRR with continuous compounding benefits.

- Traditional PE funds: Historical 12-18% IRR over full fund lifecycle.

- Public market alternatives: Long-term equity returns of 8-10% annually.

Risk-Adjusted Performance Metrics:

- Enhanced portfolio stability through continuous rebalancing.

- Reduced concentration risk via diversified exposure.

- Lower volatility compared to traditional PE due to the evergreen structure.

- Improved liquidity profile without sacrificing return potential.

Fee Structure Considerations:

Semi-liquid funds typically carry management fees of 1.5-2.5% annually plus performance fees of 15-20%, which may result in higher absolute fee drag depending on performance. However, the continuous capital deployment and compounding benefits often offset these costs for long-term investors.

Democratizing Private Equity Access

The semi-liquid fund revolution is fundamentally democratizing private market access, creating a broader investor base while maintaining institutional-quality investment processes:

Enhanced Accessibility Features:

- Dramatically lower minimum investments compared to traditional funds.

- Access for registered investment advisors and wealth management platforms.

- Institutional-grade due diligence and reporting for individual investors.

- Streamlined onboarding and transparent pricing mechanisms.

Capital Stability Benefits:

- A diversified investor base reduces concentration risk.

- Individual investor "sticky" capital often exhibits lower redemption rates.

- Continuous fundraising provides steady capital inflows for opportunistic investments.

Technology Integration and Operational Excellence

Modern semi-liquid funds leverage cutting-edge technology to optimize compounding returns and operational efficiency:

Advanced Analytics Implementation:

- Real-time portfolio monitoring and performance tracking.

- Predictive modeling for market timing and asset allocation optimization.

- Automated liquidity management and redemption processing systems.

- Enhanced regulatory compliance and transparent reporting.

Digital Infrastructure Advantages:

- Streamlined investor onboarding and account management.

- Real-time NAV calculations and performance reporting.

- Enhanced transparency through digital investor portals.

- Automated compliance monitoring and audit capabilities.

Critical Success Factors and Risk Considerations

The success of semi-liquid funds hinges on several critical factors that investors must carefully evaluate:

Manager Selection:

The entire compounding advantage depends fundamentally on the manager's ability to source consistent, high-quality deal flow. Capital from realized investments must be redeployed swiftly and effectively into new portfolio companies that ultimately perform well. As one industry expert notes, "A semi-liquid fund is ultimately only as good as the assets it holds."

Valuation and Pricing Challenges:

- NAV calculations made periodically may not reflect real-time market conditions.

- Constant subscription and redemption flows can create NAV mispricing opportunities.

- Valuation lags may not capture recent market volatility fully.

- Regular fair value assessments require sophisticated valuation expertise.

Liquidity Risk Management:

- Redemptions are subject to gates during market stress periods.

- Liquidity sleeves may slightly temper overall returns.

- Not suitable for investors requiring immediate liquidity access.

- Market conditions can impact redemption timing and availability.

Regulatory Framework and Compliance Standards

Semi-liquid funds operate within established regulatory frameworks while pioneering enhanced investor protection measures:

Regulatory Structure:

- Many vehicles are registered under the Investment Company Act of 1940.

- Enhanced disclosure requirements and investor protection measures.

- Regular regulatory examinations and comprehensive reporting obligations.

- Fiduciary oversight and conflicts of interest management.

Compliance Excellence:

- Investment advisor registration and regulatory oversight.

- Best execution standards and fair dealing requirements.

- Transparent fee disclosure and performance reporting.

- Enhanced due diligence and risk management protocols.

Market Growth Trajectory and Future Outlook

The semi-liquid fund market demonstrates explosive growth driven by evolving investor preferences and technological capabilities:

Growth Statistics:

- Preqin estimates a record $350 billion in total NAV by 2024.

- Pitchbook reports $400 billion cumulative NAV since 2019.

- Annual growth rates exceeding 20% in key market segments.

- Increasing adoption by pension funds, endowments, and family offices.

Innovation Drivers:

- Blockchain technology for enhanced settlement and transparency.

- Artificial intelligence for portfolio optimization and risk assessment.

- ESG integration and impact measurement capabilities.

- Enhanced liquidity management and pricing mechanisms.

Investment Strategy Framework for Success

Maximizing compounding returns through semi-liquid funds requires a sophisticated investment strategy and rigorous manager selection:

Due Diligence Framework:

- Evaluate the management team's experience and historical track record.

- Analyze underlying portfolio composition and diversification strategy.

- Review liquidity management policies and redemption history.

- Assess fee structure competitiveness and value proposition.

Portfolio Integration Strategy:

- Allocate 10-25% of alternative investments to semi-liquid structures.

- Consider correlation with existing holdings and overall risk profile.

- Plan for long-term holding periods despite liquidity availability.

- Maintain appropriate reserves for liquidity needs outside the fund.

The Compounding Timeline: Long-Term Perspective

The true power of semi-liquid fund compounding becomes evident over extended investment horizons:

- 10-Year Compounding Impact

Using KKR's modeling, an 11.6% net IRR compounded over 10 years generates a 3x multiple, demonstrating the mathematical advantage of continuous reinvestment versus traditional distribution models. - 30-Year Wealth Creation

J.P. Morgan's analysis reveals dramatic wealth creation differentials over three decades, as the compounding engine within evergreen funds creates exponentially superior outcomes compared to traditional structures that require manual reinvestment.

Case Studies in Compounding Success

Industry leaders are demonstrating the practical application of semi-liquid fund compounding:

Institutional Validation:

- Major pension funds are allocating significant capital to evergreen structures.

- Family offices are embracing semi-liquid funds for multi-generational wealth building.

- Registered investment advisors are integrating these vehicles for client portfolios.

- Insurance companies are utilizing evergreen funds for liability matching.

Conclusion: The Evolution of Private Market Investing

Semi-liquid funds represent more than an incremental improvement in private equity access—they constitute a fundamental evolution in how institutional-quality private market returns can be delivered to a broader investor base while harnessing the mathematical power of compounding.

The evidence supports their transformative potential: over $400 billion in assets under management, mathematical advantages in compounding returns, and growing institutional adoption validate the semi-liquid fund thesis. However, success requires a sophisticated understanding of their unique characteristics, rigorous manager selection, and appropriate portfolio integration.

For investors seeking private market exposure without traditional constraints, semi-liquid funds offer a compelling pathway to participate in institutional-grade private equity growth while maintaining portfolio flexibility and enhanced liquidity access. The compounding engine they enable—through continuous capital recycling, extended investment horizons, and professional management—creates a unique value proposition that addresses the evolving needs of modern investment portfolios.

The future belongs to investment structures that combine institutional-grade returns with enhanced accessibility and flexibility. Semi-liquid funds, with their proven ability to harness compounding returns while providing periodic liquidity, represent the future today.

Frequently Asked Questions About Semi-Liquid Funds

Are Evergreen funds semi-liquid?

Yes, evergreen funds are semi-liquid. They offer quarterly or monthly redemption windows (typically 5-25% of NAV) while maintaining perpetual investment strategies. Unlike traditional PE funds with 10+ year lock-ups, evergreen funds provide periodic liquidity access.

What are types of liquid funds?

Fully Liquid: Money market funds, mutual funds, ETFs (daily access), Semi-Liquid: Interval funds, evergreen PE funds (periodic windows) Illiquid: Traditional private equity, VC funds (long-term lock-ups)

What is semi-liquid credit?

Semi-liquid credit funds invest in private credit, direct lending, and distressed debt while offering monthly or quarterly redemptions. They provide higher yields than traditional bond funds with NAV-based pricing and liquidity reserves for withdrawals.

Are interval funds semi-liquid?

Yes, interval funds are SEC-registered semi-liquid vehicles that repurchase 5-25% of shares quarterly. They invest in illiquid assets like private equity and real estate while providing predetermined liquidity windows with advance notice requirements.

What is a semi-liquid fund?

A semi-liquid fund provides periodic redemptions (quarterly/monthly) while investing in illiquid assets. Key features include:

- Limited redemption capacity (5-25% per period)

- NAV-based pricing

- Professional management

- Access to private markets

- Higher fees than traditional funds

- Not suitable for emergency liquidity needs

Pages Related to #Semi-Liquid Funds

- Wealth Building & Preservation: Investments & Loans | Paperfree

- How to Spot and Avoid Hard Money Scams

- [closed] CMF. Cedar Multifamily Fund

![[closed] CMF. Cedar Multifamily Fund](https://d2sv4n3pfes7l9.cloudfront.net/file_paperfree_144_2020-8-21-19-57-p_pf-avatar.jpg)

- EB-5 for Tech Entrepreneurs: Immigration Program for Startup Founders | Paperfree

- Indian EB-5 Golden Visa Applicants

- Fee increase for EB-5 U.S. Golden Visa 2024

- USA EB5 visa consultant

- EB-5 Project Approval Process for Regional Center Investments

Popular Page

Private Real Estate Funds - Investments to Drive Income and Capital Growth

Book a Free Complimentary Call

Search within Paperfree.com

real estate investing Investment Visa USA Investment Magazine Private Real Estate Funds real estate funds