DSCR Loans — Qualify on Rental Income, Not Your Tax Return

Paperfree DSCR loans let real estate investors grow their portfolio without W-2s, pay stubs, or personal income verification. If your property cash flows, you qualify.

.png)

Investment Opportunities

Paperfree Marketplace Private Funds

Research News and Insights

What Is a DSCR Loan?

If you're asking what a DSCR loan is, it's a type of investment property financing that qualifies borrowers based on the property's rental income rather than their personal income, W-2s, or tax returns. DSCR stands for Debt Service Coverage Ratio — a measure of whether a property's rental income is sufficient to cover its debt obligations.

For anyone wondering what DSCR loans are in practical terms: they're designed specifically for real estate investors who may not show high personal income on paper — common among self-employed borrowers, investors with multiple properties, or anyone whose tax returns don't reflect their true cash flow — but whose rental properties generate solid income.

DSCR Loan Meaning

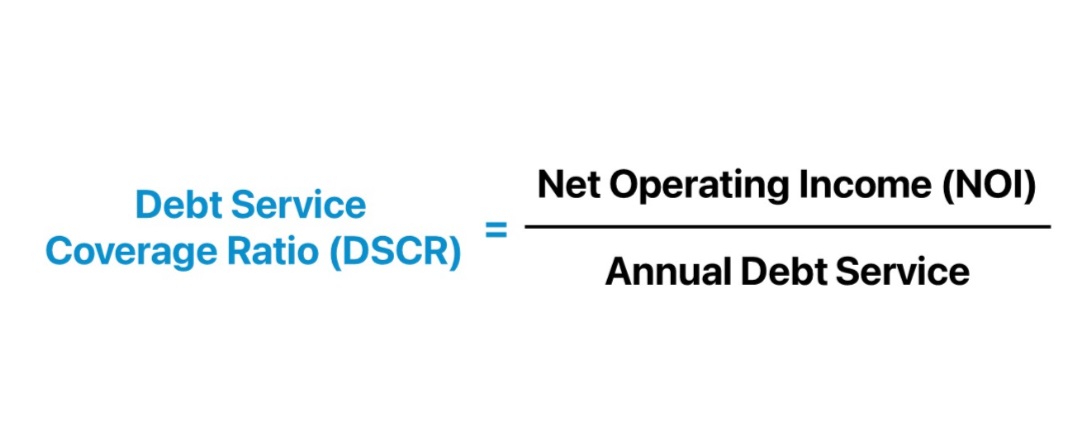

The DSCR loan meaning comes directly from the ratio lenders use to evaluate the deal: Debt Service Coverage Ratio, calculated by dividing a property's gross rental income by its total debt obligations (principal, interest, taxes, insurance). A DSCR of 1.0 means the property's rental income exactly covers its debt payments. A DSCR above 1.0 means the property generates more income than it costs to service — the higher the ratio, the stronger the deal looks to a lender.

DSCR Loan Requirements

DSCR loan requirements differ significantly from those of a conventional mortgage. Instead of income verification, tax returns, and employment history, lenders typically evaluate:

- DSCR ratio — Most lenders look for a minimum DSCR of 1.0 to 1.25, though some programs allow lower ratios with tradeoffs like a higher rate or larger down payment

- Property type — Single-family rentals, multi-family properties, and short-term rentals may all qualify, depending on the lender

- Down payment — Typically 20-25% of the purchase price

- Credit score — Most programs require a minimum credit score, though requirements are generally more flexible than conventional financing

- Property appraisal and rental income analysis — Used to confirm the property can support the loan based on actual or projected rental income

How to Get a DSCR Loan

If you're figuring out how to get a DSCR loan, the process is more streamlined than conventional financing:

- Identify or already own a rental property with strong cash flow potential

- Get a rental income analysis or appraisal to establish the property's DSCR

- Provide basic documentation — no tax returns or W-2s required

- Receive loan terms based on the property's DSCR and your down payment

- Close and fund, often faster than a traditional income-verified mortgage

How is the DSCR calculated? (formula)

Who Uses DSCR Loans

DSCR loans are especially popular among:

- Real estate investors scaling a rental portfolio who don't want their growth limited by personal debt-to-income ratios

- Self-employed borrowers whose tax returns understate their actual income

- Investors purchasing through an LLC or other business entity

- Buy-and-hold investors executing a BRRRR strategy who need to refinance quickly based on the property's new rental income

Get Started

If your property cash flows, you may already qualify. Contact us today to see what DSCR loan terms your investment property can support.

Free Consultation